Social Security benefits are a cornerstone of retirement planning for many Americans. Understanding how and when to claim these benefits is crucial for maximizing retirement income.

Navigating the complexities of Social Security can seem daunting, but it’s essential for ensuring a stable financial future. These benefits, funded by payroll taxes, are designed to replace a portion of your pre-retirement income based on your lifetime earnings. The age at which you choose to start receiving your benefits can significantly impact your monthly payments.

Early retirement can reduce your benefits, while delaying your claim can increase them. This makes it important to strategize your claim to optimize your retirement income. With proper planning and understanding of Social Security rules, you can make informed decisions that enhance your financial security in your golden years.

Introduction To Social Security And Retirement

Retirement and Social Security benefits are key to our future. It’s vital to understand how they work. This guide will help you plan your retirement with ease.

Importance Of Planning Ahead

Planning for retirement is like saving for a long vacation. You start early, save regularly, and watch your money grow. The earlier you start, the more you’ll have when you retire. This ensures a comfortable life later on.

- Start early: More time for your money to grow.

- Save regularly: Builds a habit and increases savings.

- Watch money grow: Investments and savings multiply over time.

Basics Of Social Security Benefits

Social Security is a program run by the government. It provides money to retirees, the disabled, and families of retired, disabled, or deceased workers. You earn these benefits by working and paying taxes.

| Age to Receive Full Benefits | Year of Birth |

|---|---|

| 67 | 1960 or later |

| 66 and certain months | 1943-1959 |

Remember, you can start receiving benefits at age 62. But, your monthly check will be smaller. Waiting until full retirement age or longer increases your benefits.

- Apply online or in person.

- Provide necessary documents.

- Receive benefits monthly.

Eligibility Criteria For Social Security Benefits

Understanding the eligibility criteria for Social Security benefits is crucial. It helps plan for a secure retirement.

Qualifying For Benefits

Before reaping Social Security rewards, individuals must earn them. This involves acquiring sufficient work credits. Work credits are the benchmark used by the Social Security Administration (SSA) to determine eligibility. They reflect an individual’s work history and contributions to Social Security through taxes.

Earn credits by working and paying Social Security taxes. In 2023, one credit equals $1,510 in earnings. Earn up to four credits per year.

Workers need 40 credits to qualify, typically 10 years of work. Younger workers may qualify for disability or survivor benefits with fewer credits.

| Years of Work | Credits Earned | Benefits Eligibility |

|---|---|---|

| 10+ | 40+ | Full |

| Under 10 | Less than 40 | Limited |

Age Considerations

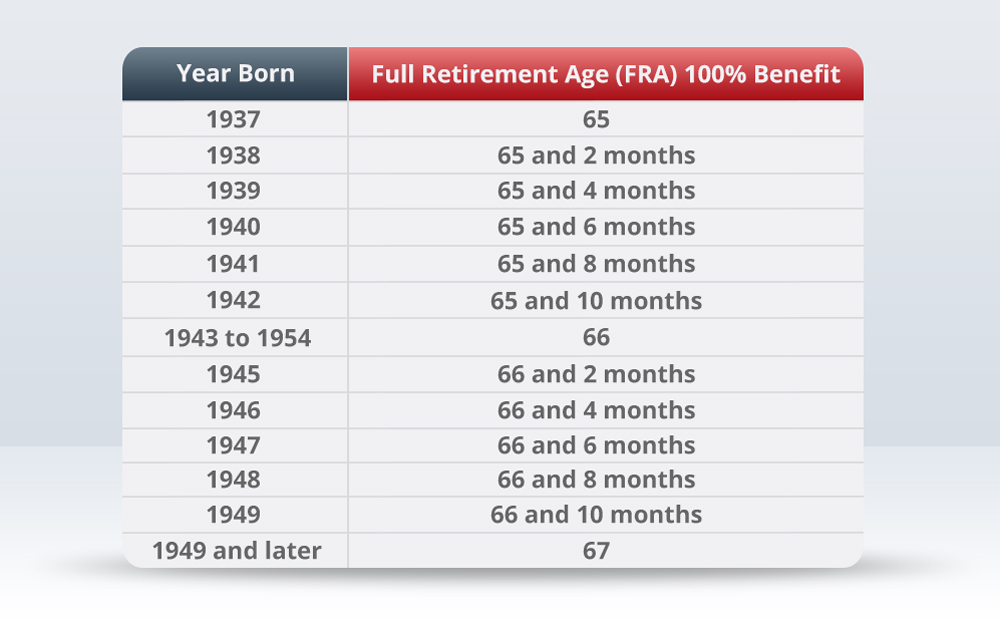

Age plays a pivotal role in determining when individuals can receive full Social Security benefits. Known as the full retirement age (FRA), it varies depending on the birth year.

- Before 1954: FRA is 66

- 1955 to 1959: FRA increases gradually

- 1960 or later: FRA is 67

Starting benefits before FRA results in lower monthly payments. Conversely, delaying benefits past FRA increases monthly payments.

Individuals can start receiving benefits as early as age 62. But waiting until 70 maximizes the payout.

Maximizing Social Security Benefits

Understanding how to maximize Social Security benefits is vital for retirement planning. It ensures a stable income later in life. Knowing the best strategies can lead to higher payouts. Let’s explore these strategies.

Strategies For Higher Payouts

Smart moves can boost Social Security checks. Here are top strategies:

- Work at least 35 years to ensure a higher calculation base.

- Delay benefits past full retirement age for an increase.

- Check records for accuracy to avoid missing out on funds.

- Maximize earnings during working years to up your benefit.

- Coordinate with spouse for optimal claiming strategies.

Timing Your Claim

Choosing when to claim benefits impacts monthly checks. Consider these points:

| Age | Impact on Benefits |

|---|---|

| 62 years | Early claiming reduces checks. |

| Full Retirement Age | Full benefits based on work record. |

| 70 years | Max increase in benefits reached. |

Delaying claims can lead to larger benefits. This suits those with longer life expectancies. Claiming early may fit others with different needs. Each person’s situation dictates the best time to claim.

Retirement Savings Beyond Social Security

Many people plan for retirement with Social Security benefits in mind. Yet, relying solely on Social Security might not suffice for a comfortable retirement. It’s wise to explore additional avenues to ensure financial stability. Let’s dive into some key options for retirement savings beyond Social Security.

401(k) And Ira Accounts

Employer-sponsored 401(k) plans are a popular choice for retirement savings. Employees contribute pre-tax dollars, reducing taxable income. Many employers match a portion of these contributions, boosting the retirement fund. To maximize benefits, aim for the highest match percentage.

Individual Retirement Accounts (IRAs) offer another savings route. Traditional IRAs provide tax-deferred growth, while Roth IRAs offer tax-free withdrawals in retirement. Both account types have annual contribution limits and offer various investment options.

Other Investment Options

Diversification is key in building a robust retirement portfolio. Consider these investment options:

- Stocks: Potential for high returns but come with higher risk.

- Bonds: Offer steady income with lower risk than stocks.

- Mutual Funds: Pool money with other investors to buy a portfolio of stocks or bonds.

- Real Estate: Can provide rental income and property value appreciation.

- Certificates of Deposit (CDs): Low-risk savings option with fixed interest rates.

Consider consulting a financial advisor to tailor your investment strategy to your goals and risk tolerance. Start early, stay consistent, and review your plan regularly for best results.

The Role Of Pensions And Annuities

As we approach retirement, understanding the role of pensions and annuities is crucial. Both can provide a stable income stream. It’s important to know how they work and which is best for you.

Understanding Pension Benefits

Pensions are retirement plans funded by employers. They promise a fixed monthly income after retirement. The benefit amount usually depends on salary and years of service.

- Employer-funded: Your company handles contributions.

- Guaranteed income: You get a set amount each month.

- Based on service: The longer you work, the more you get.

Many pensions are insured by the PBGC, ensuring payments even if the company fails.

Choosing The Right Annuity

An annuity is a contract with an insurance company. You make a lump-sum payment or a series of payments. In return, you receive regular disbursements.

| Type | Features |

|---|---|

| Immediate | Payments start soon after purchase. |

| Deferred | Payments begin at a future date. |

| Fixed | Provides a guaranteed payout. |

| Variable | Payouts can fluctuate with market performance. |

Choosing the right annuity depends on your financial goals and needs. Speak with a financial advisor to make an informed decision.

Healthcare Considerations In Retirement

Retiring means thinking about your health needs. Healthcare considerations in retirement are crucial. You might need more medical care as you age. This section talks about how to plan for those needs.

Medicare And Medicaid

Medicare is a program for people over 65 or with certain disabilities. It helps cover some healthcare costs. Medicaid helps people with limited income and resources. It covers some costs not paid by Medicare. It’s important to know:

- Medicare Part A covers hospital stays.

- Part B covers doctor visits and tests.

- Part D helps pay for prescriptions.

- Medicaid eligibility varies by state.

Sign up for Medicare before turning 65 to avoid penalties.

Long-term Care Insurance

Some retirees might need long-term care. This care is not always covered by Medicare or Medicaid. Long-term care insurance can help. It covers services like:

- Home care

- Assisted living

- Nursing home care

Buying a policy early can reduce costs. It’s a key step in retirement planning.

Tax Implications For Retirees

Understanding the tax implications for retirees is crucial. Social Security benefits often represent a significant portion of retirement income. Taxes on these benefits can impact retirees’ financial health.

Social Security Benefit Taxes

Retirees must consider taxes on Social Security benefits. Not all retirees pay taxes on Social Security. Taxes depend on ‘combined income’.

Combined income includes adjusted gross income, nontaxable interest, and half of Social Security benefits. Singles with combined income between $25,000 and $34,000 may pay taxes on up to 50% of benefits. For income above $34,000, up to 85% of benefits may be taxable.

Married couples face different thresholds. They pay taxes on up to 50% of benefits with combined income between $32,000 and $44,000. Above $44,000, up to 85% of their benefits may be taxable.

Efficient Tax Planning

Efficient tax planning can reduce taxes on Social Security benefits. This involves managing income streams and understanding tax brackets.

Retirees should consider the timing of withdrawing from retirement accounts. This can affect taxable income levels. Distributions from IRAs or 401(k)s increase taxable income. This can push combined income above Social Security tax thresholds.

Strategic withdrawals from retirement accounts may keep income below tax thresholds. This requires careful planning and possibly consulting a tax professional.

Investing in tax-efficient vehicles like Roth IRAs can benefit retirees. Roth IRA withdrawals do not count towards combined income. This helps keep Social Security benefits tax-free.

Retirees should also consider state taxes. Some states tax Social Security benefits, while others do not. Knowing state laws can help in planning for tax efficiency.

Credit: www.londoneligibility.com

Estate Planning And Beneficiaries

Understanding estate planning and beneficiaries is crucial when discussing Social Security benefits and retirement. It ensures your assets pass on as intended. Let’s explore key elements like wills, trusts, and managing inheritance.

Wills And Trusts

Estate planning starts with a will or trust. A will outlines your wishes. A trust offers more control over assets. Both secure your legacy and protect beneficiaries.

- Wills ensure assets distribution per your desires.

- Trusts manage assets for beneficiaries’ benefits.

- Choose executors and trustees wisely.

Managing Inheritance

Properly managing inheritance maintains financial stability for heirs. Educate beneficiaries about their future assets. Consider trust funds for minors or spendthrift trusts for those needing financial oversight.

- Discuss inheritance details with heirs.

- Set up trusts for minors or financially inexperienced beneficiaries.

- Regularly review and update beneficiary designations.

Lifestyle Changes And Budgeting

Retirement brings significant lifestyle and financial changes. Planning for a new budget on a fixed income is vital. Let’s explore strategies to manage your finances post-retirement.

Adjusting To A Fixed Income

Retirement income often means less money each month. It’s important to review and adjust spending. Start by categorizing expenses. Create a budget that fits your new income. Cutting non-essential costs helps. Focus on needs over wants. Be mindful of each dollar spent.

Cost Of Living Adjustments

Social Security may offer Cost of Living Adjustments (COLAs). COLAs help your benefits keep pace with inflation. Watch for annual COLA announcements. They affect your budget. A small increase can help cover rising costs. Remember, COLAs are not guaranteed each year.

Plan for lifestyle changes early. Embrace budgeting as a tool. It’s key to a comfortable retirement. Live within your means. Seek ways to stretch your dollars. Retirement can be a joyful phase with smart financial moves.

Credit: www.simplywise.com

Staying Informed And Adapting To Changes

Understanding Social Security benefits is crucial for a secure retirement. Laws and policies often change. Keeping up with these updates can impact your financial planning. Let’s explore how you can stay informed and adapt to changes efficiently.

Keeping Up With Policy Changes

- Subscribe to official newsletters.

- Follow trusted news sources.

- Attend community seminars.

- Use government websites for accurate information.

Timely knowledge of policy shifts helps you make better decisions. It ensures that you maximize your benefits.

Continuous Financial Review

Regularly check your financial status. Adjust your plans as needed.

| Year | Estimated Benefits | Action Needed |

|---|---|---|

| 2023 | $1,500/month | Review investment portfolio |

| 2024 | $1,550/month | Check policy updates |

| 2025 | $1,600/month | Adjust savings contributions |

Update your budget with the latest benefit figures. Seek professional advice when necessary. This ensures that your retirement savings are on track.

Credit: www.elderneedslaw.com

Frequently Asked Questions

Can You Get Retirement Benefits And Social Security At The Same Time?

Yes, you can receive retirement benefits and Social Security simultaneously. Eligibility depends on your age and work history. Ensure to check specific requirements, as combining benefits may affect the total amount received. Always consult with the Social Security Administration for personalized advice.

How Much Do You Get For Retirement From Social Security?

Social Security retirement benefits vary based on your work history and the age you retire. The average monthly payment is around $1,500. Your specific amount depends on your earnings record and retirement age. To get an accurate estimate, use the Social Security Administration’s online calculator.

What Is The 10 Year Rule For Social Security?

The 10-year rule for Social Security requires 40 credits, typically 10 years of work, to qualify for retirement benefits.

What Is The Difference Between Social Security And Retirement Benefits?

Social Security is a federal program providing various benefits, while retirement benefits specifically refer to financial support given after leaving the workforce.

Conclusion

Navigating the intricacies of Social Security can profoundly impact your golden years. Planning ahead ensures you maximize your benefits, securing a comfortable retirement. Stay informed, prepare early, and consider professional advice to optimize your financial future. Remember, a strategic approach to Social Security is key to a fulfilling retirement.