Retirement planning for the self-employed involves setting aside funds and choosing the right savings plan. It’s crucial to start early for a secure future.

Navigating the world of retirement planning as a self-employed individual can seem daunting. Unlike traditional employees, who might have access to employer-sponsored retirement plans, entrepreneurs and freelancers must take the initiative to plan for their retirement. This process demands a strategic approach to selecting the best retirement savings options, such as SEP IRAs, Solo 401(k)s, and Simple IRAs.

These options not only help in building a retirement corpus but also offer tax advantages. Effective retirement planning enables self-employed individuals to enjoy financial security in their later years, ensuring that they can maintain their desired lifestyle without the need for active income. Starting this planning process early maximizes the potential for compound growth, making it easier to achieve retirement goals.

The Importance Of Retirement Planning For Self-employed Individuals

Retirement planning is crucial for self-employed individuals. Unlike traditional employees, self-employed professionals must tackle retirement planning on their own. This means setting aside funds, choosing investments, and planning for taxes without the guidance of an employer-sponsored plan. Recognizing the importance of retirement planning can secure a stable financial future.

Challenges Unique To The Self-employed

- No employer-sponsored retirement plans.

- Irregular income streams make saving difficult.

- Higher tax responsibilities with less guidance.

- Must self-manage retirement funds and investments.

Self-employed individuals face unique challenges in saving for retirement. Without the cushion of employer contributions, they must navigate the complexities of investing and saving independently. This requires discipline and a strong understanding of financial planning.

Benefits Of Proactive Retirement Planning

- Financial Security: Ensures a stable income in retirement.

- Tax Benefits: Contributions to retirement accounts can reduce taxable income.

- Control Over Investments: Freedom to choose where to invest retirement savings.

- Peace of Mind: Reduces stress knowing retirement is secure.

Proactive retirement planning empowers self-employed individuals. It offers financial security and peace of mind. By understanding and overcoming unique challenges, self-employed professionals can enjoy the benefits of a well-planned retirement.

Starting Points For Retirement Savings

When it comes to retirement savings, knowing where to start is key. Self-employed individuals face unique challenges in this journey. But with the right strategy, they can create a robust retirement plan. Let’s explore some foundational steps to set the stage for a secure future.

Assessing Current Financial Health

Understanding your financial situation is crucial. Look at income, expenses, debts, and savings. A clear financial picture helps with planning.

- Analyze monthly cash flow.

- Check debt levels.

- Calculate net worth.

Tools like spreadsheets or apps can track these figures effectively.

Setting Retirement Goals

Setting goals gives direction to saving efforts. Consider lifestyle, desired retirement age, and income needs.

- Define a retirement age.

- Estimate future expenses.

- Plan for healthcare costs.

Use online calculators to estimate the savings required to meet these goals.

Retirement Account Options For The Self-employed

Planning for retirement is crucial, especially for the self-employed. Many self-employed individuals overlook the importance of retirement savings. Yet, a variety of retirement account options exist, tailored to their unique needs. Let’s explore the accounts that can help secure a financially stable future.

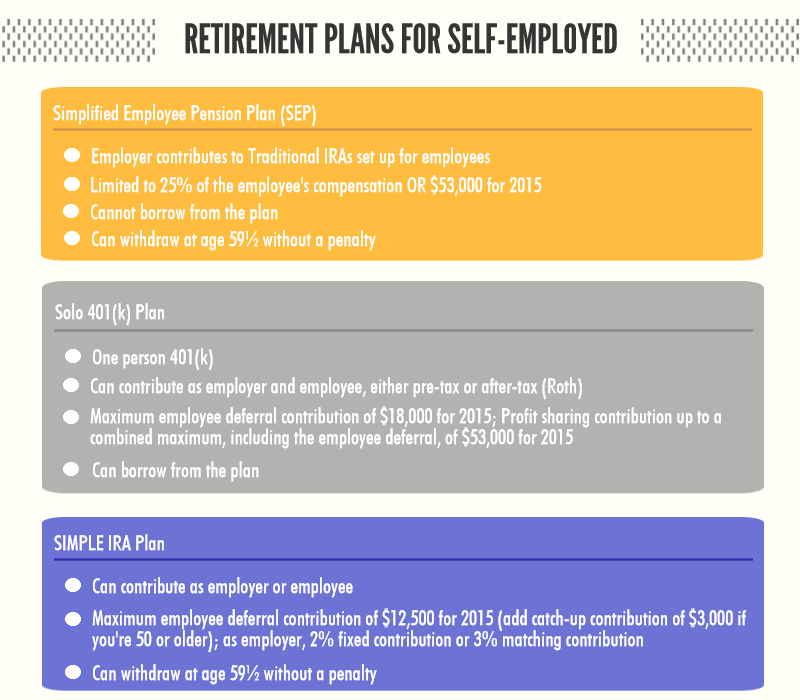

Solo 401(k) Plans

A Solo 401(k) is a powerful tool for self-employed individuals. It allows large annual contributions. Both employee and employer contributions are possible, boosting your savings pot. This plan is best for those with no employees, excluding a spouse.

- High contribution limits

- Tax-deferred growth

- Potential for a Roth option

Sep Iras

SEP IRAs offer simplicity and flexibility. They are ideal for solopreneurs or small business owners. Contributions are tax-deductible, and the setup process is straightforward. This plan works well for those who prefer less paperwork.

| Features | Benefits |

|---|---|

| Easy to set up and maintain | Reduces administrative burden |

| Flexible annual contributions | Adjust as income fluctuates |

Simple Iras

The SIMPLE IRA is great for growing businesses. It suits those with up to 100 employees. Employers must contribute, and employees can too. This plan promotes shared responsibility towards retirement savings.

- Allows employee contributions

- Requires employer matching

- Good for small businesses

Understanding Tax Implications

Self-employed individuals must grasp how taxes affect their retirement savings. Knowing the rules can lead to smarter decisions and more savings for the golden years. Let’s dive into the tax nuances that every self-employed person should be aware of.

Deductible Contributions

Contributions to certain retirement accounts are tax-deductible. This means you can deduct the money you put into a retirement account from your income. Doing so lowers your taxable income and, therefore, your tax bill for the year.

- IRA contributions can reduce taxable income

- SEP-IRA and Solo 401(k) plans offer higher contribution limits

Tax-deferred Growth

With tax-deferred accounts, you pay no taxes on earnings until you withdraw them. This allows your investments to grow without the drag of taxes, compounding your earnings over time.

- Traditional IRAs and 401(k)s offer tax-deferred growth

- No taxes on dividends or capital gains until withdrawal

Roth Options And Post-tax Benefits

Roth accounts are funded with post-tax dollars. This means you pay taxes on your contributions now. However, withdrawals in retirement are tax-free, including the earnings.

| Roth IRA | Roth 401(k) |

|---|---|

| No up-front tax deduction | Higher contribution limits than Roth IRA |

| Tax-free withdrawals in retirement | No income limits for contributions |

Investment Strategies For Retirement Portfolios

Self-employed professionals face unique challenges in retirement planning. Unlike traditional employees, they lack access to employer-sponsored retirement plans. Thus, robust investment strategies become crucial. Smart asset allocation and risk management ensure a stable financial future.

Asset Allocation And Diversification

Asset allocation involves spreading investments across various asset classes. Diversification reduces risk and improves potential returns. A well-diversified portfolio includes stocks, bonds, and real estate. It may also feature alternative investments like commodities or private equity.

Key points for asset allocation:

- Balance between growth and income

- Vary investment types

- Rebalance annually

Diversification protects against market volatility. It helps smooth out investment returns over time.

Risk Management Over Time

Risk management adapts as individuals approach retirement. Younger self-employed professionals can take more risks. They have time to recover from market downturns. As retirement nears, reducing risk becomes vital.

Consider these steps:

- Review risk tolerance regularly

- Shift towards bonds and fixed-income assets

- Plan for long-term care needs

Effective risk management ensures that retirement savings last. It also provides peace of mind during market swings.

Credit: 401kcalculator.net

Insurance And Healthcare Considerations

Insurance and Healthcare Considerations are vital for self-employed individuals. Planning for healthcare needs is a must. This ensures a safe and secure retirement.

Health Insurance Options

Choosing the right health insurance is key. Many options exist for self-employed professionals. Let’s explore:

- Marketplace Plans: Shop for plans on the government’s marketplace. You might get a subsidy.

- Professional Associations: Some offer members health insurance.

- Health Sharing Plans: A less traditional route. Members share healthcare costs.

Each option has pros and cons. Think about your health needs and budget.

Long-term Care Insurance

What happens if you need long-term care? Medicare might not cover it all. Long-term care insurance can help.

| Option | Benefits | Considerations |

|---|---|---|

| Traditional LTC Insurance | Covers most long-term care costs | Can be expensive as you age |

| Hybrid LTC Insurance | Combines life insurance with LTC benefits | More flexible but higher initial cost |

Think about your future needs. Start planning early to save money.

Estate Planning And Legacy Building

When it comes to retirement planning, many self-employed individuals focus on saving and investment strategies. But a key aspect often overlooked is estate planning and legacy building. This ensures your wealth transfers according to your wishes. Addressing estate planning early can secure your legacy and provide peace of mind.

Creating A Will

A will is a legal document. It outlines who will inherit your assets. Without a will, state laws decide. This may not reflect your wishes. Creating a will allows you to designate heirs for your business and personal assets. You can also name guardians for minor children. This is a vital step in estate planning.

Trusts And Wealth Transfer

Trusts serve multiple purposes in estate planning. They offer control over asset distribution. They can also reduce estate taxes. Trusts and wealth transfer involve setting up legal entities. These hold assets for your beneficiaries. You decide when and how they receive these assets. Trusts can protect your legacy from creditors and legal disputes.

- Revocable trusts let you change terms any time.

- Irrevocable trusts do not allow changes once established.

- Living trusts become effective during your lifetime.

- Testamentary trusts are set up in a will and take effect after death.

Credit: www.consumerscu.org

Seeking Professional Advice

Retirement planning can seem daunting, especially for the self-employed. Without the support of an employer’s pension scheme, it’s crucial to get expert advice. A financial advisor or retirement coach can provide tailored strategies to secure your future. Let’s explore when and why to seek their guidance.

When To Consult A Financial Advisor

Starting early is key in retirement planning. But certain life events make consulting a financial advisor even more important:

- Major income changes: When your earnings rise or fall significantly.

- Business growth: If your business expands, affecting your financial landscape.

- Approaching retirement: Ideally, meet an advisor ten years before retiring.

- Life milestones: Marriage, children, or buying a home can impact retirement plans.

The Role Of Retirement Coaches

A retirement coach focuses on the non-financial aspects of retiring:

| Area | How a Coach Helps |

|---|---|

| Transition | Guides through the shift from work life to retirement. |

| Lifestyle planning | Helps envision and plan your desired retirement lifestyle. |

| Emotional support | Provides support for the emotional journey of retiring. |

Retirement coaches complement financial advisors. They help you adjust to the new phase of life. Start with a financial advisor, then consider a retirement coach for holistic planning.

Adapting Plans To Changing Circumstances

Life changes, and so must retirement plans for the self-employed. Flexibility is key. Self-employed individuals need to stay alert and responsive. This means adapting retirement strategies to fit new life circumstances. Let’s explore how to keep retirement plans dynamic and aligned with current goals.

Monitoring And Rebalancing Investments

Market conditions shift. Investments follow. Regular check-ins on investment portfolios are crucial. This ensures investments align with risk tolerance and retirement timelines. Consider these steps:

- Review investments quarterly.

- Analyze performance against benchmarks.

- Rebalance to maintain desired asset allocation.

Rebalancing can involve selling high-performing assets and buying underperforming ones. This keeps the portfolio in line with risk preferences.

Adjusting Goals With Life Changes

Life events such as marriage, children, or health issues necessitate plan adjustments. Self-employed individuals should:

- Assess new financial responsibilities.

- Update retirement savings targets.

- Consider the impact on retirement age.

Seeking advice from a financial planner can also be beneficial. This can ensure informed decisions are made. Adapting plans keeps retirement goals realistic and achievable.

Tips For Staying On Track

Self-employed professionals face unique retirement planning challenges. Unlike traditional employees, they lack access to employer-sponsored retirement plans. Tips for staying on track with retirement planning are crucial. They ensure a secure financial future. Let’s explore effective strategies.

Regular Financial Check-ups

Just like health, finances need regular check-ups. These check-ups help spot issues early. They also keep retirement goals in focus.

- Review savings and investment accounts often.

- Adjust contributions to match financial changes.

- Use online tools for tracking progress.

Maintaining Discipline In Saving

Saving consistently forms the backbone of a solid retirement plan. Discipline is key. It turns small savings into big nest eggs over time.

- Set clear, achievable savings goals.

- Automate savings to ensure regular contributions.

- Resist temptations to dip into retirement funds.

Credit: www.synchronybank.com

Frequently Asked Questions

Which Retirement Plan Is Best For Self-employed?

The best retirement plan for self-employed individuals often is the Solo 401(k) due to its high contribution limits and flexibility. SEP IRAs also offer simplicity and generous contribution options, making them a solid choice. Always consider personal financial goals and consult a financial advisor for tailored advice.

How Do Self-employed Prepare For Retirement?

Self-employed individuals can prepare for retirement by setting up a solo 401(k) or an IRA. Regularly contributing to these accounts is crucial. They should also diversify their investments and consider consulting a financial advisor for personalized strategies. Planning early and saving consistently are key steps for a secure retirement.

How To Plan For Retirement When You Own Your Own Business?

Start saving early by setting aside a portion of business profits. Invest in a diverse retirement portfolio. Consider a solo 401(k) or SEP IRA for tax advantages. Regularly review and adjust your retirement strategy. Seek professional financial advice to optimize your retirement plan.

How Much Should Self-employed Set Aside For Retirement?

Self-employed individuals should aim to save around 10-15% of their income for retirement, adjusting for personal financial goals and existing savings.

Conclusion

Navigating retirement planning as a self-employed individual can be challenging, yet it’s vital for a secure future. By setting clear goals, seeking professional advice, and committing to a structured savings plan, you pave the way for financial comfort in your later years.

Start planning now; your retired self will thank you.