Personal Finance Simplified: The Step-By-Step Guide for Smart Money Management explains how to effectively handle your finances. The guide offers practical tips and strategies for financial success.

Managing personal finances can seem overwhelming. Breaking it down into manageable steps makes the process easier and less intimidating. This guide covers everything from budgeting and saving to investing and debt management. Understanding these principles helps you make informed financial decisions.

Start with setting clear financial goals. Track your income and expenses to identify spending patterns. Create a realistic budget that aligns with your goals. Prioritize paying off high-interest debts to reduce financial stress. Build an emergency fund to handle unexpected expenses. Investing wisely grows your wealth over time. This guide provides the tools you need for smart money management.

Credit: www.goodreads.com

Introduction To Personal Finance

Personal finance is all about managing your money. It involves budgeting, saving, investing, and planning for the future. Understanding personal finance helps you make smart financial decisions. It can lead to financial independence and a secure future.

Why Personal Finance Matters

Managing your money wisely is crucial. It helps you achieve your financial goals. Whether it’s buying a home, saving for education, or planning for retirement. Personal finance ensures you have enough funds for emergencies. It can reduce stress and improve your quality of life.

Here are some reasons why personal finance matters:

- Financial Security: Proper management ensures you have a safety net.

- Goal Achievement: Helps you reach personal and financial milestones.

- Debt Management: Keeps you from accumulating bad debt.

- Improved Lifestyle: Better financial health leads to a better lifestyle.

Common Financial Pitfalls

Avoiding financial mistakes is key to successful money management. Many people fall into common financial traps.

Here are some common financial pitfalls:

- Overspending: Spending more than you earn leads to debt.

- Not Saving: Lack of savings can leave you unprepared for emergencies.

- Ignoring Budgets: Not tracking expenses can result in financial chaos.

- High-Interest Debt: Credit card debt can quickly spiral out of control.

- Impulse Buying: Unplanned purchases can wreck your budget.

By understanding these pitfalls, you can take steps to avoid them. This will help you manage your money better and achieve financial stability.

Credit: www.amazon.com

Setting Financial Goals

Setting financial goals is a crucial step in smart money management. It provides a roadmap for your financial journey. Well-defined goals help you stay focused and motivated. They give you a clear vision of what you aim to achieve. Let’s break down financial goals into two categories: Short-Term Goals and Long-Term Goals.

Short-term Goals

Short-term goals are achievable within a year. These goals help you manage immediate needs and build a foundation for the future.

- Emergency Fund: Save for unexpected expenses.

- Debt Repayment: Pay off small debts quickly.

- Vacation Savings: Save for a planned trip.

Use a table to set clear short-term goals:

| Goal | Target Amount | Deadline |

|---|---|---|

| Emergency Fund | $1,000 | 6 months |

| Debt Repayment | $500 | 3 months |

| Vacation Savings | $1,500 | 12 months |

Long-term Goals

Long-term goals take more than a year to achieve. These goals are essential for your future financial security.

- Retirement Savings: Plan for a comfortable retirement.

- Home Purchase: Save for a down payment on a house.

- Children’s Education: Plan for college expenses.

Use a table to set clear long-term goals:

| Goal | Target Amount | Timeline |

|---|---|---|

| Retirement Savings | $500,000 | 20 years |

| Home Purchase | $50,000 | 5 years |

| Children’s Education | $100,000 | 15 years |

Setting clear financial goals is the first step to financial freedom. Track your progress regularly. Adjust your goals as needed.

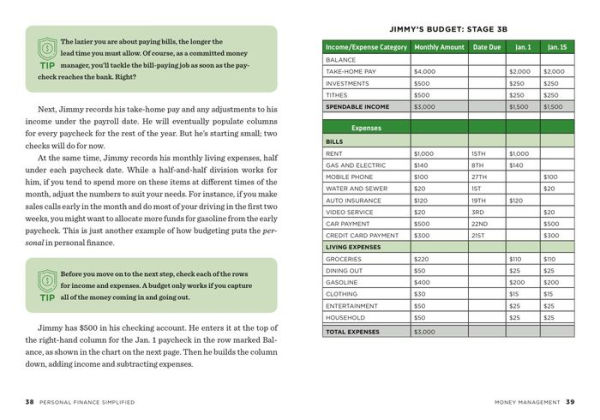

Creating A Budget

Creating a budget is essential for smart money management. A budget helps you track your income and expenses. It ensures you live within your means. This section will guide you through the process.

Tracking Income And Expenses

Start by tracking all your income sources. This includes your salary, freelance work, and any other earnings.

| Income Source | Monthly Amount |

|---|---|

| Salary | $3000 |

| Freelance | $500 |

| Other | $200 |

Next, list your monthly expenses. Include rent, utilities, groceries, and entertainment. Use a table to keep it organized.

| Expense Category | Monthly Amount |

|---|---|

| Rent | $1200 |

| Utilities | $150 |

| Groceries | $300 |

| Entertainment | $100 |

Adjusting Spending Habits

Once you know your income and expenses, adjust your spending habits. This ensures your expenses don’t exceed your income.

- Identify unnecessary expenses and cut them.

- Find cheaper alternatives for some services.

- Set savings goals and prioritize them.

Use this simple strategy to make sure you save more money:

- Track every expense daily.

- Review your spending weekly.

- Adjust your budget monthly.

By following these steps, you will master your money management. Creating a budget can be simple and effective.

Building An Emergency Fund

Managing personal finances can be challenging. A key part of smart money management is building an emergency fund. This fund acts as a financial safety net. It helps you tackle unexpected expenses without stress.

Importance Of An Emergency Fund

An emergency fund is crucial for financial stability. It helps cover sudden expenses like medical bills, car repairs, or job loss. Without it, you might need to borrow money or use credit cards. This could lead to debt and financial strain.

Consider an emergency fund as a financial cushion. It provides peace of mind and security. Knowing you have savings for emergencies reduces anxiety. You can focus on other financial goals without worry.

How Much To Save

Deciding how much to save can be tricky. Experts recommend saving at least three to six months’ worth of expenses. This amount ensures you can handle most emergencies comfortably.

Start small if saving a large amount seems daunting. Aim to save $1,000 initially. Gradually increase your savings over time. Here’s a simple table to guide you:

| Monthly Expenses | Emergency Fund Goal (3 months) | Emergency Fund Goal (6 months) |

|---|---|---|

| $1,000 | $3,000 | $6,000 |

| $2,000 | $6,000 | $12,000 |

| $3,000 | $9,000 | $18,000 |

Use these steps to build your fund:

- Set a monthly savings goal.

- Automate your savings.

- Reduce unnecessary expenses.

- Keep the funds in a separate account.

Building an emergency fund takes time and discipline. Stay consistent and patient. Your financial security will improve significantly.

Managing Debt

Debt can feel overwhelming. Managing it wisely is key to financial health. It can help you achieve financial freedom. Below, we simplify debt management. We’ll explore types of debt and strategies for paying off debt.

Types Of Debt

Understanding debt types is crucial. It helps in planning repayment strategies. Here’s a quick look:

| Type of Debt | Description |

|---|---|

| Credit Card Debt | High interest, revolving debt from credit card use. |

| Student Loans | Loans for education, usually low interest. |

| Mortgage | Loan for purchasing a home, secured by the property. |

| Auto Loans | Loan for purchasing a car, secured by the vehicle. |

| Personal Loans | Unsecured loans for various personal needs. |

Strategies For Paying Off Debt

Paying off debt requires a solid plan. Here are some effective strategies:

- Debt Snowball Method: Pay smallest debts first. Gain momentum as you go.

- Debt Avalanche Method: Pay highest interest debts first. Save on interest costs.

- Consolidation: Combine multiple debts into one. Use a lower interest rate.

- Refinancing: Replace old debt with new debt. Aim for better terms or lower interest.

- Budgeting: Create a budget. Allocate extra funds to debt payments.

Each strategy has its benefits. Choose one that fits your situation. Consistency is key. Stay committed to your plan. Track your progress regularly. Celebrate small wins. This keeps you motivated.

Investing Basics

Investing is a powerful tool for building wealth. It helps your money grow faster than just saving. Understanding the basics is essential for smart money management.

Types Of Investments

There are various types of investments. Each offers different benefits and risks.

- Stocks: Owning part of a company. Stocks can grow in value and pay dividends.

- Bonds: Loans to governments or companies. Bonds pay interest over time.

- Mutual Funds: Pools of money from many investors. Managed by professionals, they invest in stocks, bonds, or other assets.

- Real Estate: Buying property like homes or land. You can earn rental income or sell for profit.

- ETFs (Exchange-Traded Funds): Similar to mutual funds but traded on stock exchanges. They offer diversification and are usually cheaper.

Risk And Return

Every investment comes with risk and return. Knowing this helps you make better choices.

| Investment Type | Risk Level | Potential Return |

|---|---|---|

| Stocks | High | High |

| Bonds | Medium | Medium |

| Mutual Funds | Medium | Medium to High |

| Real Estate | Medium | High |

| ETFs | Low to Medium | Medium |

Higher risk usually means higher potential return. Lower risk means lower potential return. Balance risk and return based on your goals and comfort level.

Retirement Planning

Planning for retirement is crucial for a secure future. Effective retirement planning helps ensure financial stability. It allows you to enjoy your golden years stress-free. This section will guide you through key aspects of retirement planning.

Retirement Accounts

Retirement accounts are essential for saving money for the future. They offer tax benefits and help your savings grow over time. There are different types of retirement accounts:

- 401(k): Offered by employers, contributions are pre-tax.

- IRA: Individual Retirement Account, available to anyone with earned income.

- Roth IRA: Contributions are post-tax, but withdrawals are tax-free.

- Pension Plans: Employer-funded, providing regular income after retirement.

Each account type has unique benefits. Choose the one that fits your needs best. Start contributing early to maximize growth.

Planning For Different Stages Of Life

Retirement planning varies at different life stages. Here are some strategies for each stage:

| Life Stage | Strategy |

|---|---|

| 20s and 30s |

|

| 40s and 50s |

|

| 60s and Beyond |

|

Each stage requires different actions. Stay proactive and adjust your plan as needed. Regularly review your progress to stay on track.

Credit: www.barnesandnoble.com

Protecting Your Finances

Protecting your finances is crucial for long-term financial health. This section will guide you through essential steps to safeguard your money. Learn about insurance essentials and identity theft protection to keep your finances secure.

Insurance Essentials

Insurance is a key component of financial protection. It helps cover unexpected costs that could drain your savings. Here are the must-have insurance types:

- Health Insurance: Covers medical expenses, reducing financial strain during illnesses.

- Life Insurance: Provides financial support to your family if you pass away.

- Auto Insurance: Protects against vehicle-related damages and liabilities.

- Home Insurance: Covers damages to your home and possessions.

Having these insurances can save you from huge expenses. They offer peace of mind and financial stability.

Identity Theft Protection

Identity theft is a growing threat. Protecting your identity is as important as protecting your money. Follow these steps to safeguard yourself:

- Monitor Your Accounts: Regularly check your bank and credit accounts for suspicious activity.

- Use Strong Passwords: Create complex passwords for online accounts. Avoid using the same password for multiple sites.

- Enable Two-Factor Authentication: Adds an extra layer of security to your accounts.

- Shred Sensitive Documents: Properly dispose of documents containing personal information.

Protecting your identity prevents financial loss and stress. Stay vigilant and take proactive steps to secure your personal information.

Review And Adjust

Managing money is not a one-time task. Regularly reviewing and adjusting your finances helps you stay on track. It ensures your money works best for you. Let’s dive into how you can do this effectively.

Regular Financial Checkups

Just like your health, your finances need regular checkups. Schedule a monthly or quarterly review of your budget. This helps you see where your money goes. Identify unnecessary expenses and cut them out.

- Check your bank statements.

- Review your credit card bills.

- Analyze your savings and investments.

Make adjustments to your budget as needed. This keeps you on track with your financial goals.

| Time Period | Financial Checkup Tasks |

|---|---|

| Monthly | Review budget, bank statements, and credit card bills |

| Quarterly | Analyze savings, investments, and adjust budget |

Adapting To Life Changes

Life changes can impact your finances. Be ready to adapt. Major life events like getting married, having a baby, or changing jobs require financial adjustments.

- Reevaluate your budget.

- Adjust your savings goals.

- Update your insurance policies.

- Plan for future expenses.

Being proactive helps you handle these changes smoothly. Stay flexible and adjust your plans as needed.

Key Takeaway: Regularly review and adjust your finances. This ensures you stay on track with your goals. Adapt to life changes to maintain financial stability.

Frequently Asked Questions

What Is Money Management In Personal Finance?

Money management in personal finance involves budgeting, saving, investing, and spending wisely. It helps achieve financial goals and ensures stability. Effective money management reduces debt and increases wealth.

How Do I Set Up Money Management?

Set financial goals and create a budget. Track expenses and income. Save regularly and invest wisely. Avoid unnecessary debt. Monitor progress monthly.

What Is The First Step In Managing Personal Finance?

The first step is creating a detailed budget. Track your income and expenses to understand your financial situation.

How Can I Save More Money Effectively?

To save more, automate your savings. Set up a monthly transfer to your savings account to ensure consistency.

Conclusion

Mastering personal finance can lead to a stress-free life. By following these steps, you can achieve financial stability. Remember, smart money management is a continuous journey. Keep learning and adapting. Stay committed to your financial goals, and you will see rewarding results.

Your future self will thank you.