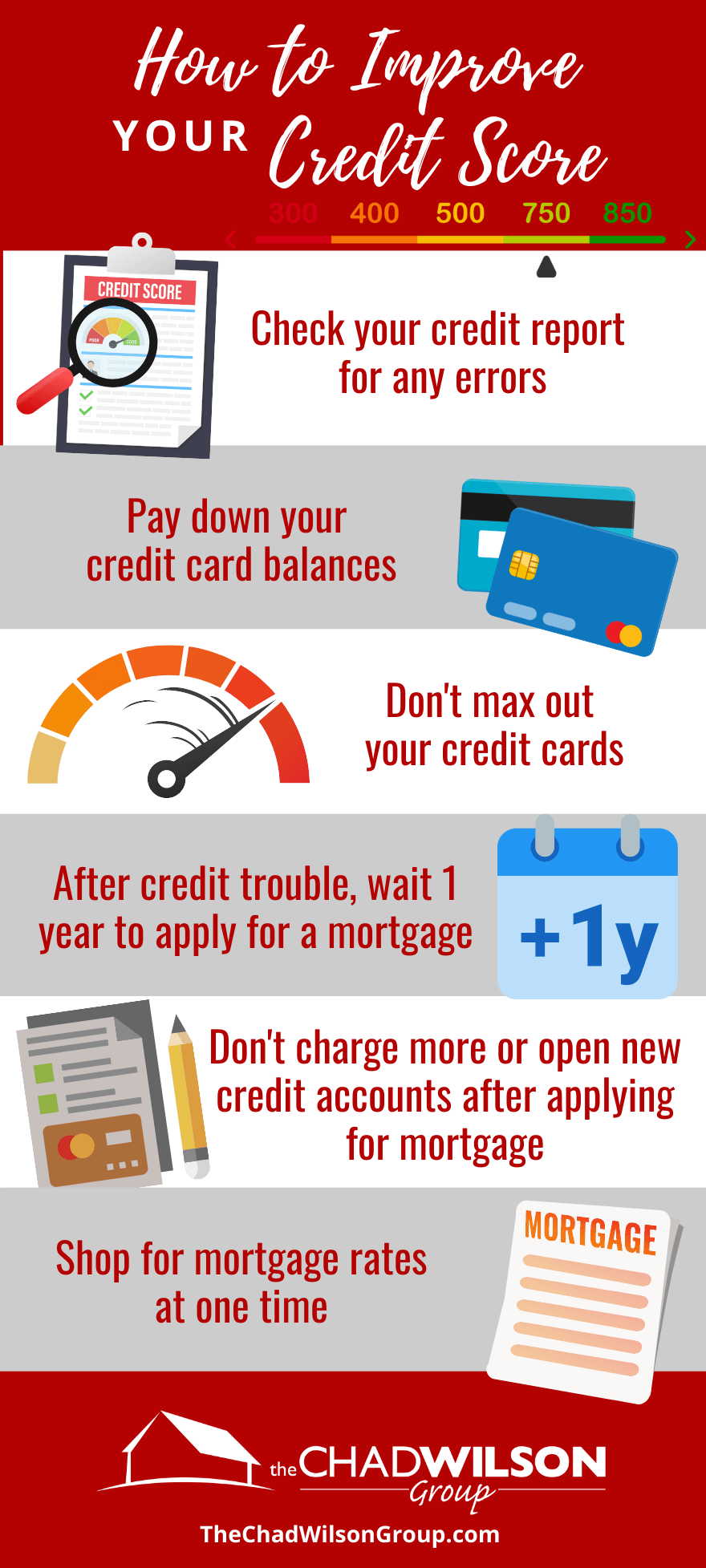

To improve your credit score, pay bills on time and reduce outstanding debt. Regularly check your credit report for errors.

Your credit score plays a crucial role in your financial health. It affects your ability to secure loans, credit cards, and even housing. Building a good credit score takes time and consistent effort. Start by making timely payments on all your bills.

Reduce your credit card balances to lower your debt-to-income ratio. Regularly monitor your credit report to identify and correct any errors. Avoid opening too many new accounts at once, as this can lower your score. Practice responsible credit habits to see gradual improvements. A higher credit score can unlock better financial opportunities for you.

Credit: www.thechadwilsongroup.com

Assessing Your Current Score

Before you can improve your credit score, you need to know where you stand. This means assessing your current credit score. Understanding your score is the first step to financial health. Follow the steps below to start your journey to a better credit score.

Checking Credit Reports

Your credit report holds all your financial history. It shows your payment history, amounts owed, and more. You can get free credit reports from annualcreditreport.com. Check your reports from all three major bureaus:

- Equifax

- Experian

- TransUnion

Look for errors or outdated information. Incorrect data can harm your score. If you find any errors, file a dispute with the credit bureau. Fixing these mistakes can quickly boost your score.

Understanding Credit Scores

Credit scores range from 300 to 850. A higher score means better creditworthiness. The score is made up of several factors:

| Factor | Percentage |

|---|---|

| Payment History | 35% |

| Amounts Owed | 30% |

| Length of Credit History | 15% |

| New Credit | 10% |

| Types of Credit Used | 10% |

Your payment history is the most important factor. Always pay your bills on time. Keep your credit card balances low. The length of your credit history also matters. The longer your history, the better.

Be cautious with new credit. Applying for many new accounts can lower your score. Diverse types of credit, like credit cards and loans, can help your score. Mix up your credit types for a better score.

By checking your reports and understanding your score, you can start making improvements. Small steps can lead to big changes in your credit health.

:max_bytes(150000):strip_icc()/things-that-boost-credit-score-960381-v2-9599c06fcdfd4108b67a291dabd43b7d.gif)

Credit: www.thebalancemoney.com

Identifying Errors

Identifying errors in your credit report is crucial. Mistakes can lower your credit score. Regular checks help catch these errors early. This can boost your score quickly.

Common Mistakes

Several common mistakes can appear on your credit report. These errors can negatively impact your credit score. Knowing them helps you spot issues.

- Incorrect personal information

- Accounts that aren’t yours

- Duplicate accounts

- Late payments that you made on time

- Incorrect account balances

Correcting Inaccuracies

Correcting inaccuracies involves a few steps. First, gather your credit reports. You can get these from the three major bureaus: Equifax, Experian, and TransUnion.

- Review each report carefully.

- Highlight any errors you find.

- Gather evidence to support your claims.

- Contact the credit bureau to dispute the errors.

- Follow up to ensure corrections are made.

Here is a table summarizing the steps:

| Step | Description |

|---|---|

| 1 | Review each report carefully. |

| 2 | Highlight any errors you find. |

| 3 | Gather evidence to support your claims. |

| 4 | Contact the credit bureau to dispute the errors. |

| 5 | Follow up to ensure corrections are made. |

Paying Bills On Time

Paying your bills on time is crucial for a good credit score. Timely payments show that you are responsible with money. They also help avoid late fees and penalties. Here are some tips to help you never miss a payment.

Setting Reminders

Setting reminders can be very helpful. Use your phone’s calendar to set alerts. You can also use reminder apps. This helps you keep track of due dates. Write the due dates on a calendar. Place it somewhere visible, like on your fridge.

Automating Payments

Automating your payments can make life easier. Most banks offer this service. Set up automatic payments for your bills. This ensures you never miss a payment. Just make sure there is enough money in your account.

Here’s how to set up automatic payments:

- Log in to your bank account online.

- Find the bill pay section.

- Add the bill you want to automate.

- Set the amount and date for the payment.

- Confirm the setup.

Automatic payments save time and reduce stress. They help improve your credit score by ensuring timely payments.

Reducing Debt

Reducing debt can greatly improve your credit score. You can do this by creating a payment plan and consolidating debt. These methods help manage your finances better.

Creating A Payment Plan

Making a payment plan is important. Start by listing all your debts. Include amounts and due dates. Use a table to organize this information:

| Debt Type | Amount | Due Date |

|---|---|---|

| Credit Card | $2,500 | 15th of the Month |

| Student Loan | $10,000 | 1st of the Month |

| Car Loan | $5,000 | 20th of the Month |

Next, set a budget. Prioritize your debts. Pay off high-interest debts first. This strategy saves money in the long run.

Use automatic payments. This ensures you never miss a payment. Missing payments can harm your credit score.

Consolidating Debt

Debt consolidation can simplify your payments. This means combining multiple debts into one.

Here are some methods for consolidating debt:

- Balance Transfer Credit Card: Transfer all your debts to one card. Look for a card with low-interest rates.

- Personal Loan: Get a loan to pay off your debts. Then, pay back the loan in installments.

- Home Equity Loan: Use the equity in your home to consolidate debt. This often has lower interest rates.

Debt consolidation can make managing your debt easier. It often results in lower monthly payments. This can free up money for other uses.

Before consolidating debt, check the terms. Some methods have fees. Make sure the benefits outweigh the costs.

Using Credit Responsibly

Improving your credit score starts with using credit responsibly. This means making smart choices about how you handle your credit accounts. It involves keeping your credit card balances low and avoiding new credit applications. Let’s dive into these strategies.

Keeping Balances Low

Keeping your balances low is crucial. High balances can hurt your credit score. Aim to use less than 30% of your credit limit.

| Credit Limit | Recommended Balance |

|---|---|

| $1,000 | Under $300 |

| $5,000 | Under $1,500 |

| $10,000 | Under $3,000 |

Pay off your balances each month. This shows lenders you are responsible. If you can’t, pay more than the minimum.

Use your credit cards for small purchases. This helps keep your balances low.

Avoiding New Credit

Avoiding new credit applications is important. Each application can lower your credit score.

- Each application triggers a hard inquiry.

- Hard inquiries can lower your score by a few points.

Only apply for new credit if you really need it. Too many new accounts can make you look risky.

Keep your existing accounts open. Closing accounts can hurt your score.

Focus on using your existing credit wisely. This will help your score improve over time.

Building Credit History

Building a strong credit history is essential for a good credit score. A good credit score helps you get better interest rates on loans and credit cards. Here are some effective ways to build your credit history:

Opening New Accounts

Opening new credit accounts can help build your credit history. When you open a new account, it adds to your credit mix. This can improve your credit score over time. Here are some tips for opening new accounts:

- Start with a secured credit card. These cards require a deposit, which acts as your credit limit.

- Apply for a retail store card. These cards are often easier to get approved for.

- Consider a credit-builder loan. These loans help you build credit by making small, regular payments.

Make sure to use new accounts responsibly. Pay your bills on time and keep your balances low.

Becoming An Authorized User

Becoming an authorized user on someone else’s credit card can also help build your credit history. When you become an authorized user, the account’s history appears on your credit report. Here’s how to become an authorized user:

- Ask a family member or close friend with good credit.

- Ensure the primary cardholder pays their bills on time.

- Check if the credit card issuer reports authorized user activity to credit bureaus.

Being an authorized user can help build your credit history without the responsibility of managing an account.

Monitoring Progress

Monitoring your credit score progress is essential. It helps you see improvements and identify issues. By keeping an eye on your credit score, you stay informed.

Regular Credit Checks

Regular credit checks are vital. They help you spot errors and fraud. You should check your credit report every few months. This ensures your information is accurate. Use trusted sources like Equifax, Experian, and TransUnion.

Here is a simple table to understand the frequency of checks:

| Frequency | Action |

|---|---|

| Monthly | Basic monitoring |

| Quarterly | Detailed review |

| Yearly | In-depth analysis |

Tracking Score Improvements

Tracking score improvements keeps you motivated. You see the results of your hard work. Use tools like credit score trackers. Many banks offer free tracking services.

Here are some steps to track your score:

- Enroll in a credit monitoring service.

- Set up alerts for changes.

- Review your credit report regularly.

- Note any score changes.

- Adjust your financial habits accordingly.

By following these steps, you ensure continuous improvement. Always aim for a higher score.

Credit: www.welchstatebank.com

Seeking Professional Help

Seeking professional help can be a smart move to improve your credit score. Experts can offer tailored advice and strategies to boost your score. Here, we discuss two primary options: credit counseling services and financial advisors.

Credit Counseling Services

Credit counseling services provide expert advice on managing your credit. They help you understand your credit report and identify areas for improvement. Many credit counseling agencies offer free initial consultations.

- Budget Planning: Counselors help create a realistic budget.

- Debt Management: They offer strategies to manage and reduce debt.

- Credit Education: Learn how to use credit responsibly.

These services often negotiate with creditors to lower interest rates. This can make your debt more manageable.

Financial Advisors

Financial advisors offer comprehensive financial planning. Their services go beyond just improving your credit score. They help with investment strategies, retirement planning, and more.

- Personalized Advice: Advisors offer tailored financial plans.

- Long-Term Planning: They focus on your long-term financial health.

- Investment Guidance: Advisors help you make wise investment choices.

Hiring a financial advisor can be costly. However, their expertise can provide significant long-term benefits. They offer strategies that go beyond credit improvement, ensuring overall financial well-being.

Frequently Asked Questions

What Is The Fastest Way To Boost Credit Score?

Pay down credit card balances, correct errors on your credit report, and avoid late payments. Minimize new credit applications.

What Is The Fastest Way To Fix Your Credit Score?

Pay your bills on time and reduce credit card balances. Dispute errors on your credit report. Avoid new credit inquiries.

What Are 3 Things You Can Do To Improve Your Credit Score?

1. Pay bills on time to build a positive payment history. 2. Keep credit card balances low to reduce credit utilization. 3. Regularly check credit reports for errors and dispute inaccuracies.

How To Get A 720 Credit Score In 6 Months?

Pay bills on time, reduce credit card balances, avoid new credit inquiries, maintain old accounts, and monitor your credit report.

Conclusion

Boosting your credit score takes time and effort. Pay bills on time and reduce debt. Regularly monitor your credit report for errors. Small steps lead to significant improvements. A better credit score opens doors to financial opportunities. Start today and see positive changes.