Budgeting strategies for families focus on managing expenses and saving for the future. Effective planning enables financial stability and growth.

Crafting a budget is a critical step for any family aiming to maintain financial health. It’s not just about tracking where money goes each month but also about setting and achieving financial goals. A well-structured budget helps in identifying unnecessary expenses, allocating funds for emergencies, and planning for both short-term and long-term objectives.

This approach fosters a sense of security, reduces financial stress, and promotes a healthier economic environment within the household. By adhering to a budget, families can enjoy a more organized financial life, paving the way for savings, investments, and ultimately, financial independence. The key lies in understanding income, managing expenses wisely, and making informed decisions that contribute to a family’s overall financial well-being.

The Importance Of Family Budgeting

Family budgeting plays a crucial role in managing household finances. It helps families plan expenses and save for the future. Understanding the importance of a structured budget can lead to financial stability and peace of mind.

Creating A Financial Foundation

A solid financial foundation is key for any family. It starts with a clear budget. This plan shows income, expenses, and savings. Families can track their spending habits. They learn where they can cut costs. This leads to more savings.

- Track all expenses to see where money goes.

- Identify needs versus wants to reduce unnecessary spending.

- Set financial goals for both short-term and long-term.

Benefits Of A Structured Budget

A structured budget offers many benefits. It brings financial discipline. Families avoid debt by living within their means. They save for emergencies and future goals.

| Benefit | Description |

|---|---|

| Control Over Finances | Know exactly where each dollar is going. |

| Reduces Stress | Less worry about money with a clear plan. |

| Saves Money | Identify and cut unnecessary expenses. |

With a budget, families work together towards financial success. They make informed decisions about spending and saving. Everyone understands the family’s financial goals. This unity is the foundation of a healthy financial future.

Assessing Your Current Financial Situation

Assessing your current financial situation is a critical first step. It lays the groundwork for effective budgeting. Understanding where money comes from and where it goes is key. Let’s dive into how families can track their finances accurately.

Tracking Income And Expenses

Start by recording every dollar earned and spent. This gives a clear picture of your financial health. Use tools or apps to simplify this process.

- List all income sources

- Record all bills and daily expenses

- Review bank statements regularly

Identifying Financial Leaks

Financial leaks drain budgets without notice. Spotting them early stops waste and saves money.

| Common Financial Leaks | Solutions |

|---|---|

| Unused subscriptions | Cancel them |

| Eating out often | Cook at home more |

| Impulse shopping | Stick to a shopping list |

Review expenses to find patterns. Cut back on non-essential spending. Put the saved money towards goals.

Setting Realistic Financial Goals

Managing money wisely is key for family happiness. Setting realistic financial goals guides your spending and saving. It helps to secure your family’s future. Let’s explore how to set goals that work.

Short-term Vs Long-term Goals

Knowing the difference is vital. Short-term goals are for immediate needs. They include weekly groceries or a family outing. Long-term goals focus on the future. Think college funds or a new home. Both need clear timelines and a solid plan.

Involving The Whole Family

Money matters are a team effort. Discuss goals with everyone. Even kids can learn about saving. Create a budget together. Track progress as a family. Celebrate when you reach goals. This builds good habits for life.

Credit: www.psecu.com

Crafting A Family Budget That Works

Creating a budget is essential for financial health. Families need a plan that fits their unique needs. A well-crafted family budget helps manage expenses, save for the future, and reduce stress. Let’s explore strategies to build a budget that aligns with family goals.

Allocating Funds Wisely

Track all expenses to see where money goes. List income sources to understand total earnings. Prioritize spending to cover essentials first. This includes housing, food, utilities, and education. Allocate funds for savings and unexpected costs. Use a spending plan to guide purchases and avoid overspending.

- Housing: Mortgage or rent, property taxes, home insurance.

- Food: Groceries, dining out, school meals.

- Utilities: Electricity, water, gas, internet.

- Education: Tuition, books, supplies.

- Savings: Emergency fund, retirement, college fund.

Flexible Budgeting Techniques

Flexibility in budgeting allows for changes in income and expenses. Use digital tools to adjust budgets quickly. Allocate extra funds to savings or debt when possible. Set aside a small budget for fun activities to keep morale high. Teach kids about money with an allowance system. This prepares them for future financial decisions.

- Choose a budgeting app or software.

- Review and adjust the budget monthly.

- Plan for holidays, vacations, and birthdays.

- Involve the whole family in financial discussions.

- Reward savings milestones to encourage good habits.

Money-saving Tips For Everyday Expenses

Managing a family budget can be a challenge. Yet, smart strategies can lead to significant savings. Below are key tips for reducing everyday expenses. These ideas help families keep more money in their pockets.

Smart Grocery Shopping

Strategic planning before grocery shopping saves money. Here are some tips:

- Create a meal plan – Plan weekly meals to avoid buying unnecessary items.

- Use a shopping list – Stick to a list to prevent impulse purchases.

- Buy in bulk – Purchase larger quantities of non-perishable items to save in the long run.

- Choose store brands – Opt for generic brands that often cost less than name brands.

- Look for discounts – Use coupons, loyalty programs, and shop during sales.

Cutting Utility Costs

Utility bills can drain your budget. Use these tips to reduce costs:

- Switch off appliances – Turn off devices not in use to lower energy bills.

- Use energy-efficient bulbs – Replace old bulbs with LED ones for longer life and less power use.

- Seal leaks – Fix any leaks in doors or windows to save on heating and cooling.

- Lower water heating temperature – Reduce the setting to save energy and still enjoy hot showers.

- Install a programmable thermostat – Control heating and cooling for when you need it most.

Teaching Kids About Money Management

Teaching Kids About Money Management is a vital skill for families. It helps children understand the value of money. They learn to save, spend wisely, and make smart financial decisions. This section covers key strategies to teach kids about managing money effectively.

Age-appropriate Financial Lessons

Children’s ability to grasp financial concepts grows as they age. Tailoring lessons to their developmental stage ensures they understand and retain the information.

- 3-5 years old: Introduce basic concepts like saving coins in a piggy bank.

- 6-10 years old: Explain the idea of earning money through chores.

- 11-13 years old: Discuss budgeting, saving for goals, and basic banking.

- 14+ years old: Teach about credit, investments, and more complex financial planning.

Making Saving Fun For Children

Encouraging kids to save money doesn’t have to be boring. Turn it into a fun activity!

- Create a savings goal chart that they can color in as they save.

- Offer small rewards for reaching savings milestones.

- Use interactive apps designed to teach kids about saving and budgeting.

These methods make saving exciting. They teach kids the joy of reaching financial goals.

Planning For Big-ticket Purchases

Big-ticket purchases can be daunting for families. A clear plan ensures these buys do not disrupt your finances. Consider items like cars, home renovations, or vacations. Planning helps you enjoy these without worry.

Avoiding Debt Traps

Big purchases should not lead to debt. It’s tempting to use credit cards or loans. Yet, this can lead to long-term financial stress. Families should plan to avoid these traps.

- Review your budget before you commit to a big buy.

- Compare prices and options to find the best deal.

- Think about future costs that come with your purchase.

Savi

ng Strategies For Major Expenses

Start saving early for big items. This approach reduces financial pressure later. Let’s look at strategies that work.

- Create a savings goal for your item.

- Open a dedicated savings account for this purpose.

- Set up automatic transfers to this account each month.

Saving can be easier with a clear plan. For example, let’s say a family wants a new car. They decide it will cost $20,000. They plan to buy in 5 years. They need to save $333 each month. This plan makes the goal achievable.

| Car Price | Time Frame | Monthly Savings |

|---|---|---|

| $20,000 | 5 Years | $333 |

Credit: oklahomamoneymatters.org

Emergency Funds And Financial Security

Emergency funds act as a financial safety net. They help families handle sudden expenses. Without an emergency fund, unexpected events can lead to debt. Financial security means being ready for these surprises.

Building A Safety Net

Start with small savings goals. Aim to save a bit from each paycheck. Over time, this grows into a substantial fund. A good target is enough to cover three to six months of living expenses. This money should stay easily accessible.

- Open a dedicated savings account

- Set a monthly saving goal

- Automate transfers to your emergency fund

- Review and adjust goals as needed

Insurance As A Protective Measure

Insurance protects against large, unexpected costs. It covers health, home, and auto emergencies. Families should choose plans that balance coverage with affordable premiums. This ensures peace of mind.

| Insurance Type | Purpose | Note |

|---|---|---|

| Health Insurance | Covers medical bills | Choose a plan with comprehensive coverage |

| Homeowners/Renters Insurance | Protects your property | Ensure coverage for common local disasters |

| Auto Insurance | Covers vehicle-related damages | Consider coverage for uninsured motorists |

Remember, an emergency fund and proper insurance are keys to financial security. They protect against life’s unexpected turns. Start building your safety net today. Ensure your family’s future is secure.

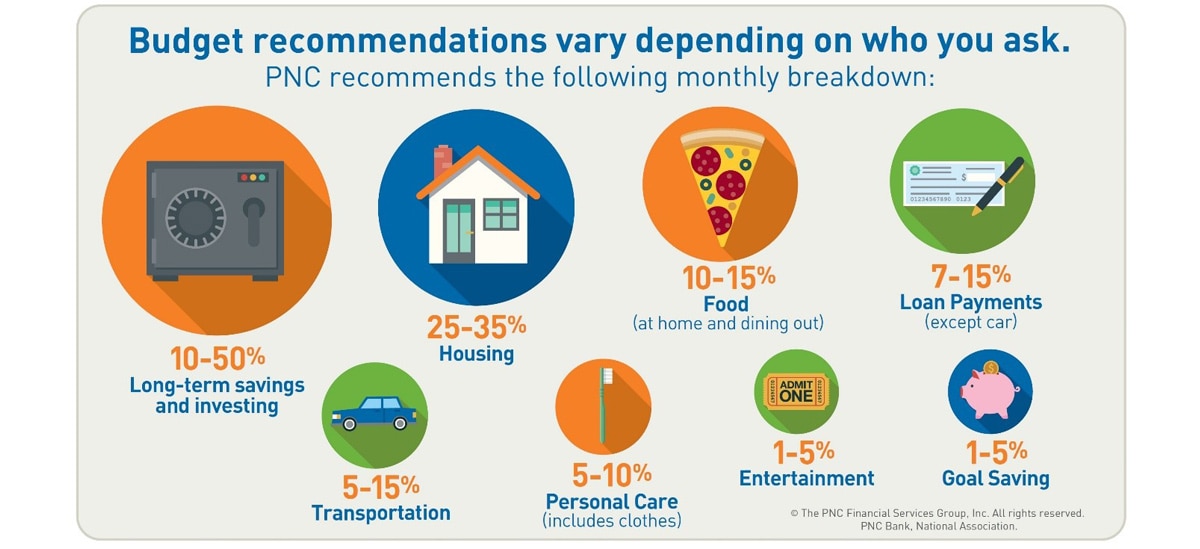

Tools And Apps To Simplify Budgeting

Tools and Apps to Simplify Budgeting are essential for modern families. They help track expenses and plan finances with ease. Let’s dive into how these tools can make budgeting a breeze.

Digital Budget Planners

Digital Budget Planners offer a structured approach to managing money. They come with pre-set categories for income and expenses. This helps families see where their money goes each month.

- Plan for upcoming bills

- Set savings goals

- Adjust budgets quickly

Expense Tracking Applications

Expense Tracking Applications focus on daily spending. They often sync with bank accounts for real-time updates. This provides a clear picture of financial habits.

- Monitor account balances

- Track spending trends

- Receive alerts for unusual activity

Credit: www.pnc.com

Adapting Budget Plans To Changing Circumstances

Adapting Budget Plans to Changing Circumstances is crucial for family financial stability. Life is unpredictable. Jobs change. Costs rise and fall. A budget must be flexible to survive these waves.

Dealing With Income Fluctuations

Income can vary, and budgets need to reflect this. Families may face layoffs, reduced hours, or seasonal work. It’s vital to adjust spending to match current income levels. Here are strategies to manage these changes:

- Track income monthly to see trends.

- Set aside savings during high-income months.

- Review and adjust expenses regularly.

Budgeting During Economic Downturns

Economic downturns demand smart budgeting. Prices may rise, and jobs might be scarce. Here’s what families can do:

- Prioritize expenses: Focus on needs over wants.

- Seek deals: Use coupons, sales, and discounts.

- Reduce costs: Cut back on non-essential services.

Remember, a budget is a living document. It grows and changes with your family’s needs.

Frequently Asked Questions

What Is The Most Effective Way To Manage A Family Budget?

The most effective way to manage a family budget involves tracking expenses, setting clear financial goals, and regularly reviewing spending habits. Implement a budgeting tool or app for easier monitoring. Prioritize savings by allocating funds to an emergency account each month.

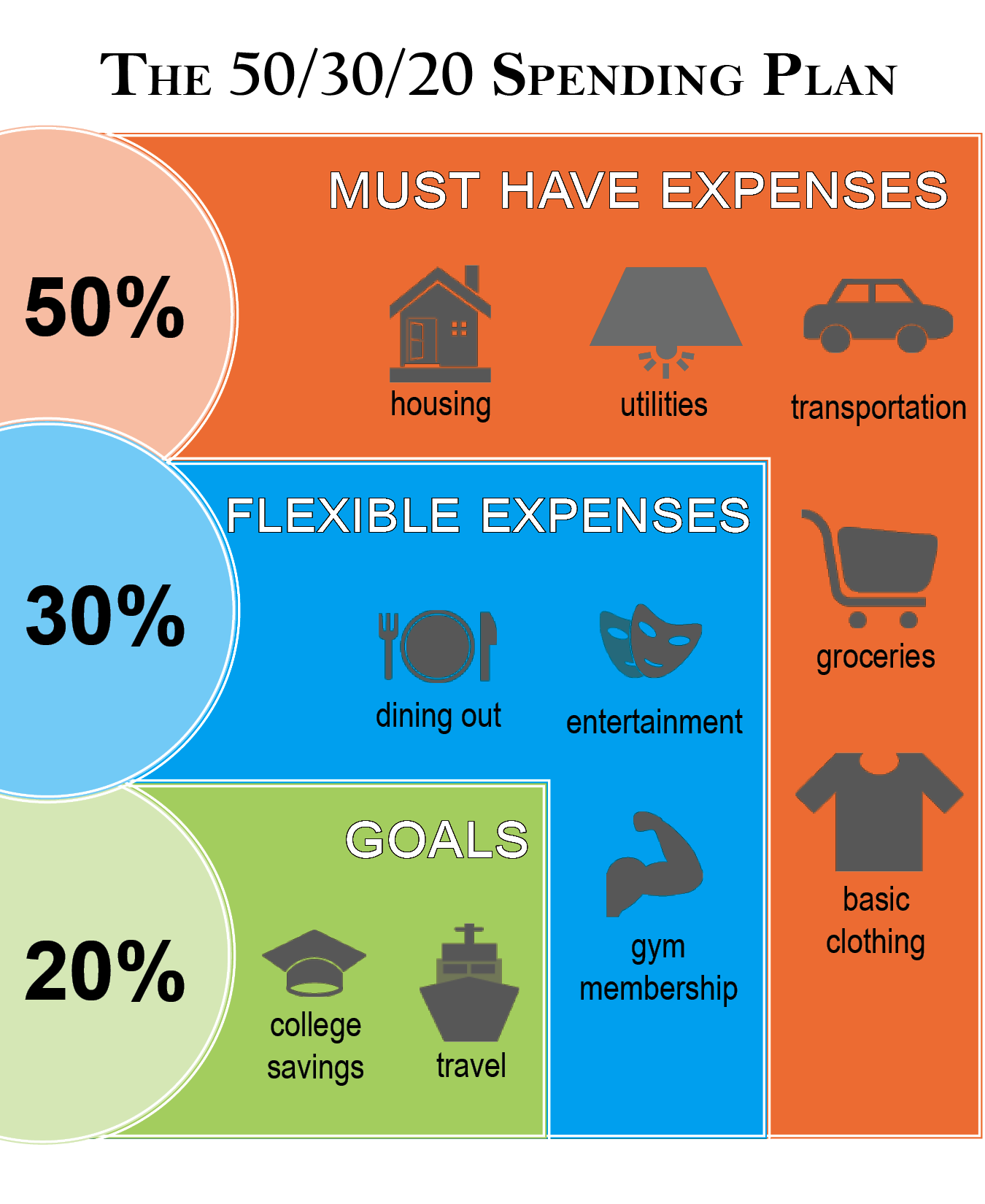

What Is The 50 30 20 Budget Rule For Kids?

The 50 30 20 budget rule for kids teaches financial management by dividing money into categories: 50% for needs, 30% for wants, and 20% for savings. This simple strategy encourages smart spending and saving habits from a young age, making it an effective tool for financial education.

What Is The Best Way To Do A Household Budget?

Start by tracking your income and expenses. Categorize spending and set realistic limits. Prioritize savings, and review your budget monthly to adjust for changes. Use budgeting tools or apps for convenience and accuracy.

Which Type Of Budget Is Best For A Family?

The best budget for a family is zero-based budgeting, where every dollar is allocated to a specific expense, ensuring clear financial planning and spending control.

Conclusion

Embracing effective budgeting strategies is vital for family financial health. By prioritizing expenses, setting realistic goals, and involving every family member, you create a sustainable financial future. Remember, successful budgeting is a journey that fosters security and peace of mind for your loved ones.

Start today, and watch your family thrive.