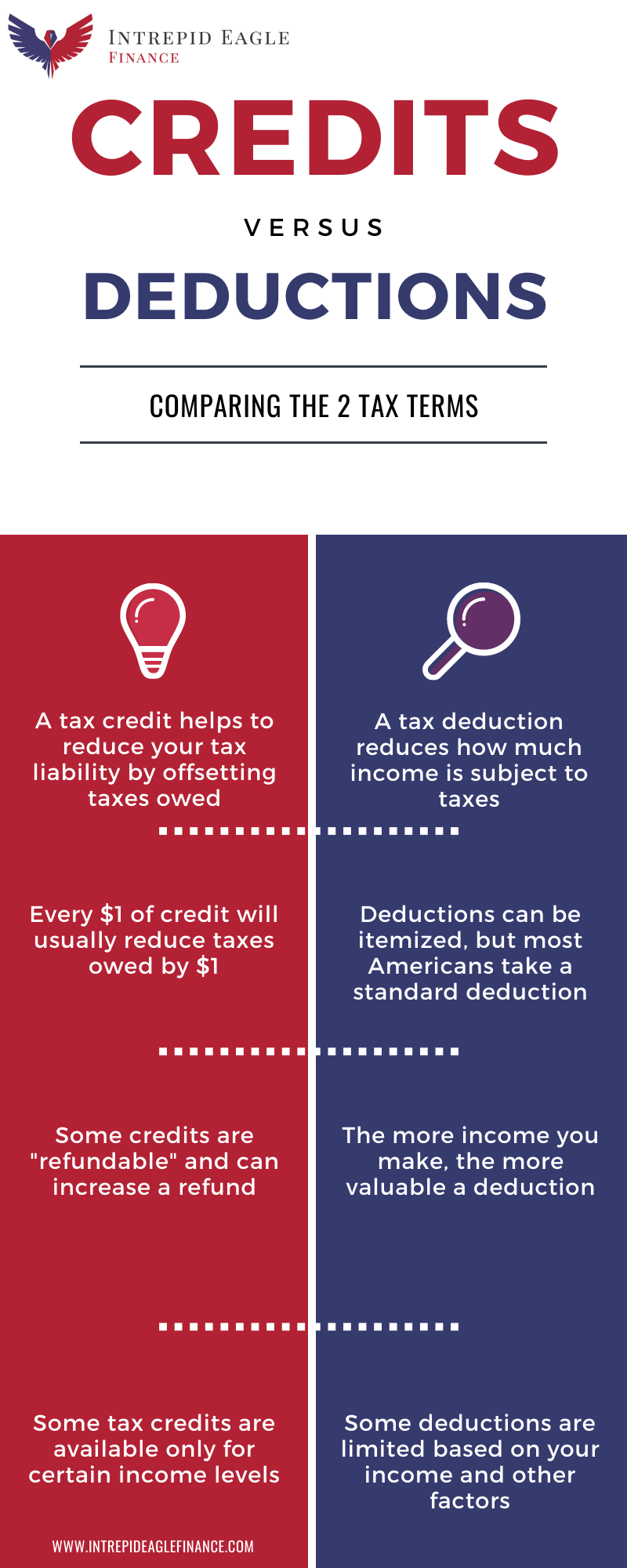

A tax credit directly reduces the amount of tax owed. A tax deduction lowers taxable income.

Understanding the difference between tax credits and deductions is crucial for effective tax planning. Tax credits provide a dollar-for-dollar reduction in your tax liability. They are more beneficial than deductions because they directly decrease the amount of tax you owe.

Tax deductions, on the other hand, reduce your taxable income. This means you pay tax on a smaller amount of your income. Knowing how each works can significantly impact your tax return. For instance, a $1,000 tax credit saves you $1,000 in taxes, whereas a $1,000 deduction might save you $250 if you’re in a 25% tax bracket. Effective use of both can maximize your tax savings.

Tax Credit Basics

Understanding tax credit basics can save you money. Tax credits reduce the amount you owe in taxes. They are different from tax deductions, which lower your taxable income. Below, we’ll explore the fundamentals of tax credits.

Definition Of Tax Credit

A tax credit directly reduces the amount of tax you owe. For example, if you owe $1,000 in taxes and have a $200 tax credit, you’ll only pay $800. Tax credits are more valuable than tax deductions because they offer a dollar-for-dollar reduction in your tax bill.

Types Of Tax Credits

There are various types of tax credits available. Each serves a different purpose and offers unique benefits.

- Nonrefundable Tax Credits: These credits can reduce your tax liability to zero but not below.

- Refundable Tax Credits: These can reduce your tax liability below zero, resulting in a refund.

- Partially Refundable Tax Credits: These credits can be partially refunded if they exceed your tax liability.

| Type of Tax Credit | Description |

|---|---|

| Nonrefundable | Reduces tax liability to zero, no further refund. |

| Refundable | Can result in a tax refund if the credit exceeds tax owed. |

| Partially Refundable | Part of the credit can be refunded, rest reduces tax liability. |

Understanding these types helps you maximize your tax savings. Use this knowledge to explore which credits you qualify for, and reduce your tax burden effectively.

Credit: quietwealth.net

Tax Deduction Fundamentals

Understanding tax deductions is vital. These deductions lower taxable income. This can reduce the amount of tax owed.

Definition Of Tax Deduction

A tax deduction is an amount that reduces your income. This means you pay tax on a smaller amount. It helps save money on taxes.

Common Tax Deductions

There are many common tax deductions. Here are a few examples:

- Mortgage interest: Interest paid on home loans.

- Charitable contributions: Donations to eligible organizations.

- Medical expenses: Costs for healthcare that exceed 7.5% of income.

- Education expenses: Tuition fees and related costs.

- State and local taxes: Including property and income taxes.

These deductions can add up. They help lower your taxable income significantly.

How Tax Credits Work

Tax credits directly reduce the amount of tax you owe. They offer significant savings compared to deductions. Understanding how tax credits work can help you maximize your tax benefits.

Eligibility Criteria

Not everyone qualifies for tax credits. Each credit has specific eligibility criteria. Here are some common factors:

- Income Level: Some tax credits target low or moderate-income earners.

- Filing Status: Your marital status can affect eligibility.

- Age: Certain credits apply to different age groups.

- Dependents: Having children or other dependents may qualify you.

- Residency: Some credits are only for residents of specific areas.

Claim Process

Claiming tax credits involves several steps. Follow this simple guide:

- Identify Eligible Credits: Determine which credits you qualify for.

- Gather Documentation: Collect necessary documents like income statements and receipts.

- Fill Out Forms: Complete the required tax forms accurately.

- Submit Your Return: File your tax return with all forms attached.

- Keep Records: Maintain copies of your submitted forms and documentation.

Here’s a table summarizing the process:

| Step | Description |

|---|---|

| Identify Eligible Credits | Determine which credits you qualify for. |

| Gather Documentation | Collect income statements and receipts. |

| Fill Out Forms | Complete the required tax forms accurately. |

| Submit Your Return | File your tax return with all forms attached. |

| Keep Records | Maintain copies of your submitted forms and documentation. |

By understanding and following these steps, you can effectively claim your tax credits and reduce your tax liability.

How Tax Deductions Work

Understanding tax deductions is essential for maximizing your tax savings. Tax deductions lower your taxable income. This reduces the amount of tax you owe. Let’s dive into how tax deductions work.

Eligibility Criteria

Not everyone qualifies for tax deductions. You must meet specific criteria.

- Income Level: Your income must fall within certain limits.

- Filing Status: Your filing status, like single or married, affects eligibility.

- Expenses: You must have qualifying expenses, like medical bills or education costs.

Claim Process

Claiming tax deductions involves several steps. Follow these steps carefully.

- Gather Documentation: Collect all receipts and records of your expenses.

- Fill Out Forms: Use IRS forms like Schedule A for itemized deductions.

- Submit with Tax Return: Attach the forms to your tax return before submission.

Understanding these basics can help you save money. Always consult with a tax professional for personalized advice.

Comparing Tax Credits And Deductions

Understanding the difference between tax credits and tax deductions can save you money. Both reduce your tax bill, but they work differently. Knowing how they impact your taxes helps you maximize savings.

Impact On Tax Liability

Tax credits directly reduce the amount of tax you owe. If you have a $1,000 tax credit, your tax bill drops by $1,000. They offer a dollar-for-dollar reduction.

Tax deductions lower your taxable income. If you have a $1,000 deduction and you’re in the 22% tax bracket, you save $220. Deductions reduce how much of your income is taxed.

Which Is More Beneficial?

To understand the benefits, let’s compare tax credits and deductions in a table:

| Aspect | Tax Credit | Tax Deduction |

|---|---|---|

| Reduction Type | Direct | Indirect |

| Impact on Tax | Dollar-for-dollar | Percentage-based |

| Example Savings | $1,000 (for $1,000 credit) | $220 (for $1,000 deduction at 22% tax rate) |

Tax credits often provide more savings. They directly cut your tax bill. Deductions only reduce taxable income, providing a smaller benefit.

Consider your tax situation carefully. Credits usually offer greater financial benefits.

Maximizing Tax Credits

Tax credits can save you a lot of money. They reduce your tax bill directly. Understanding and using these credits can make a big difference. Below are strategies for both individuals and businesses to maximize tax credits.

Strategies For Individuals

Individuals have many options to maximize their tax credits. Here are some effective strategies:

- Education Credits: The American Opportunity Credit and Lifetime Learning Credit help with education costs.

- Child Tax Credit: Parents can claim this credit for each eligible child.

- Energy-Efficient Home Improvements: Installing solar panels or energy-efficient windows can qualify for credits.

- Earned Income Tax Credit (EITC): This credit benefits low to moderate-income workers.

- Healthcare Credits: Premium Tax Credit helps cover health insurance costs for eligible individuals.

Strategies For Businesses

Businesses also have various ways to maximize tax credits. Below are some key strategies:

- Research and Development (R&D) Credit: Encourages businesses to invest in innovation.

- Work Opportunity Tax Credit (WOTC): Offers credits for hiring individuals from targeted groups.

- Energy Efficiency Credits: Businesses can claim credits for energy-saving measures.

- Small Business Health Care Credit: Helps small businesses cover employee health insurance costs.

- Disabled Access Credit: Offers credits for making your business accessible to disabled individuals.

Maximizing Tax Deductions

Understanding the difference between a tax credit and a deduction is crucial. Tax credits reduce your tax bill directly. Deductions reduce the income on which your tax is calculated. Maximizing tax deductions can save you a significant amount of money. Below, we delve into strategies and common pitfalls to help you navigate deductions efficiently.

Deduction Strategies

There are several strategies to maximize your deductions:

- Itemize Deductions: Itemizing can lead to more savings than the standard deduction.

- Track Charitable Contributions: Donations to qualified charities are deductible.

- Home Office Deduction: If you work from home, you might qualify for a home office deduction.

- Medical Expenses: Keep records of all out-of-pocket medical expenses.

- Education Expenses: Tuition and fees can sometimes be deducted.

Common Mistakes To Avoid

Avoid these common mistakes to ensure you maximize your deductions:

- Not Keeping Receipts: Always keep receipts for deductible expenses.

- Overlooking Small Deductions: Small expenses can add up. Don’t ignore them.

- Incorrectly Categorizing Expenses: Make sure expenses are categorized correctly.

- Missing Deadlines: File taxes on time to avoid penalties.

- Ignoring Professional Help: Sometimes, a tax professional can find deductions you might miss.

By following these strategies and avoiding common mistakes, you can significantly lower your taxable income. This ensures you keep more of your hard-earned money. Always stay informed and consult with a tax professional if needed.

Credit: intrepideaglefinance.com

Case Studies

Understanding the difference between a tax credit and a tax deduction can be easier with real-life examples. We will explore scenarios for individual taxpayers and small businesses. These case studies will help you grasp how each can impact your finances.

Individual Taxpayer Scenarios

Let’s look at two individuals, John and Emily, to understand tax credits and deductions.

| Aspect | John’s Scenario | Emily’s Scenario |

|---|---|---|

| Gross Income | $50,000 | $50,000 |

| Tax Deduction | $5,000 | $0 |

| Taxable Income | $45,000 | $50,000 |

| Tax Rate | 20% | 20% |

| Tax Before Credits | $9,000 | $10,000 |

| Tax Credit | $0 | $1,000 |

| Final Tax | $9,000 | $9,000 |

John benefits from a tax deduction which reduces his taxable income. Emily benefits from a tax credit which directly reduces her tax owed. Both end up paying $9,000 in taxes, but through different methods.

Small Business Scenarios

Now, let’s consider two small businesses, ABC Corp and XYZ LLC, to see the effects of tax credits and deductions.

| Aspect | ABC Corp Scenario | XYZ LLC Scenario |

|---|---|---|

| Gross Income | $200,000 | $200,000 |

| Tax Deduction | $20,000 | $0 |

| Taxable Income | $180,000 | $200,000 |

| Tax Rate | 25% | 25% |

| Tax Before Credits | $45,000 | $50,000 |

| Tax Credit | $0 | $3,000 |

| Final Tax | $45,000 | $47,000 |

ABC Corp benefits from a tax deduction which lowers its taxable income. XYZ LLC benefits from a tax credit which reduces its tax owed. ABC Corp ends up paying $45,000 in taxes, while XYZ LLC pays $47,000. These examples illustrate how both strategies can provide financial relief.

Expert Tips For Tax Savings

Understanding the difference between tax credits and tax deductions can lead to significant tax savings. This section provides expert tips to maximize your tax benefits effectively.

Consulting A Tax Professional

A tax professional can offer personalized advice. They know the latest tax laws and regulations. Their expertise ensures you don’t miss out on any benefits.

Professionals identify eligible tax credits and deductions. They help you file your taxes accurately. Mistakes can lead to penalties or lost savings.

Tax software is useful, but a human expert provides tailored advice. They can also help with tax planning for future years. This proactive approach maximizes your savings.

Staying Updated On Tax Laws

Tax laws change frequently. Staying updated ensures you benefit from new credits and deductions. Follow reputable sources like the IRS website for updates.

Subscribe to tax newsletters and alerts. They provide timely information on changes. This helps you adapt your tax strategy accordingly.

Consider taking a basic tax course. Understanding the fundamentals can enhance your tax-saving strategies. Knowledge empowers you to make informed decisions.

| Strategy | Benefit |

|---|---|

| Consult a Tax Professional | Accurate filing and personalized advice |

| Stay Updated on Tax Laws | Maximize new credits and deductions |

By following these tips, you can achieve substantial tax savings. Both tax credits and deductions offer unique benefits. Understanding them is crucial to reducing your tax burden.

Credit: intrepideaglefinance.com

Frequently Asked Questions

Is A Tax Credit Or Deduction Better?

A tax credit is usually better. It directly reduces your tax bill. Deductions lower taxable income, which might result in less savings.

Can You Claim Both Deductions And Credits?

Yes, you can claim both deductions and credits. Deductions reduce taxable income, while credits directly reduce tax owed.

What Is The Difference Between A Tax Credit And A Tax Exemption?

A tax credit reduces the amount of tax you owe. A tax exemption reduces the income subject to tax.

What Is An Example Of A Tax Credit?

A common example of a tax credit is the Earned Income Tax Credit (EITC). This credit benefits low to moderate-income workers.

Conclusion

Understanding the difference between tax credits and deductions is crucial. Tax credits directly reduce your tax bill. Deductions lower your taxable income. Both can lead to significant savings. Being informed helps you make better financial decisions. Always consult a tax professional for personalized advice.